17 / 36

17 / 36

Cushman & Wakefield

/

17

Energy-producing provinces feel the pinch

Canada’s mighty resource sector accounts for almost one-fifth of

the country’s GDP and about 1.8 million jobs. Ranked fifth in the

world in oil production, Canada produces 3.9 million bpd, 97% of

which is from Alberta, Manitoba, and Newfoundland and Labrador.

Alberta is the leading producer, responsible for almost 80% of the

country’s total output. Not surprisingly, the oil shock and sustained

low prices have weighed heavily on the most exposed office

markets of Calgary, Edmonton, and St. John’s.

Taking a heavy toll on Alberta

Calgary is home to most of Canada’s heavyweight oil and gas

companies, including EnCana, Husky Energy, and Suncor Energy.

Since late 2014, roughly 46,000 jobs have been eliminated in

Alberta due to the oil shock, and Calgary’s CBD office sector

has seen 4.3 msf of space returned to the market. Prior to the

oil price bust, Calgary boasted the highest 15-year CBD office

growth rate in the country, with 750,000 sq ft absorbed per year.

With 2.7 msf of new developments underway, the availability rate

in Calgary’s premium class A CBD buildings is projected to reach

around 27.5% by late 2017.

While Edmonton’s CBD office market has the advantage of few

significant oil tenancies, energy continues to be a key driver of

the city’s economy. Government is a major occupier of space,

and both the federal and provincial levels have been grappling

with serious shortfalls in oil and gas tax revenues since late 2014.

Against weak demand and 1.7 msf of new development in the

CBD, availability is projected to register 21.2% by Q4 2018.

St. John’s—Weathering the storm

Three billion barrels of oil and 11 trillion cubic feet of natural

gas have been discovered in Newfoundland and Labrador,

and 200,000 bpd is currently being produced from offshore

projects Hibernia, Terra Nova, and White Rose, with Hebron

under development. The economic contraction that impacted

the St. John’s office market in 2015 was due to both a 20%

drop in oil production and lower oil prices. While its CBD office

market has seen a huge slowdown in momentum, most energy

tenants are service-related, and a large proportion of them have

recently renewed their space commitments — a event which will

stabilize this market. The desire for quality space has kept Class A

availability at 8.8%, although space returning to market will push

it to 19.8% by Q4 2017.

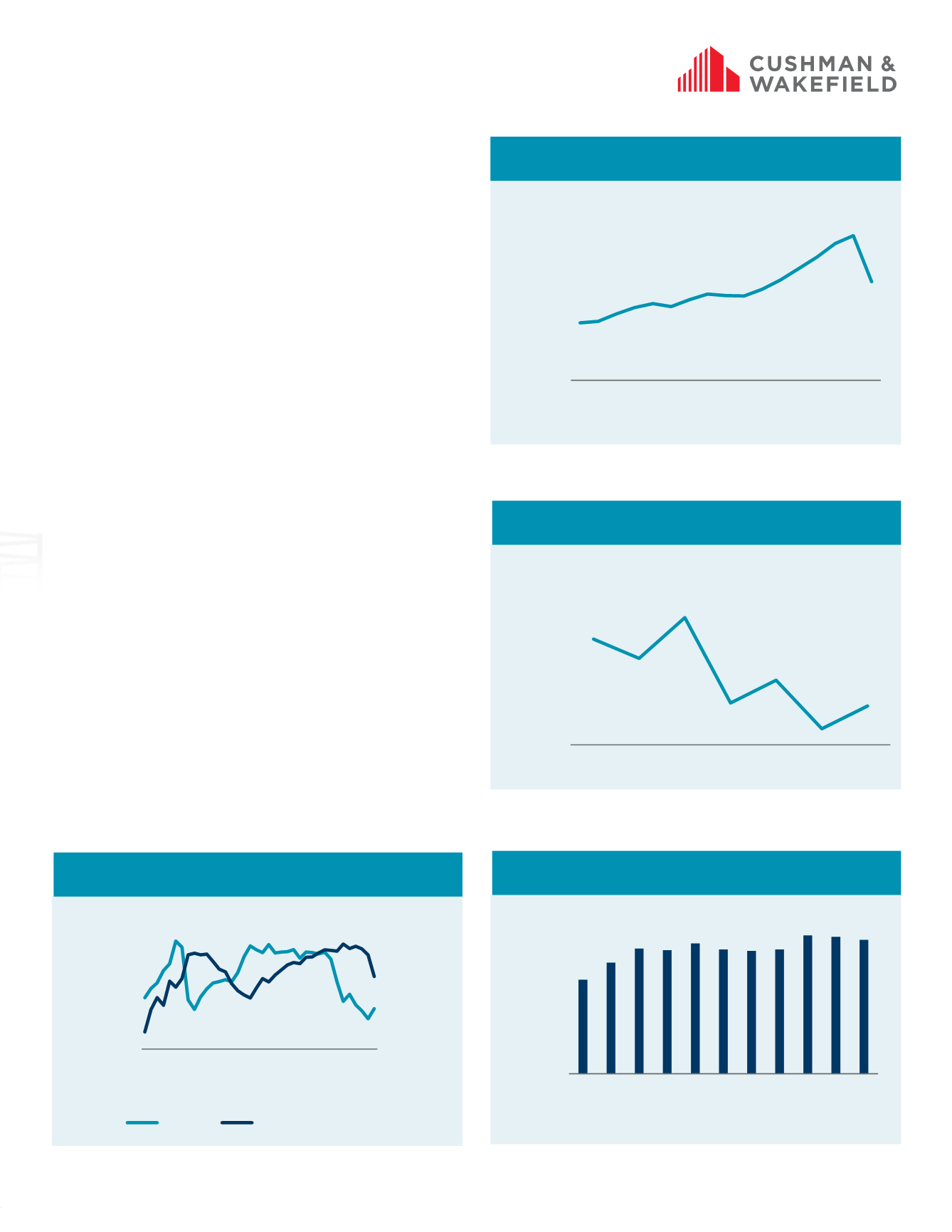

CANADIAN OIL PRODUCTION

Source: National Energy Board, Cushman & Wakefield Research

CANADIAN GAS PRICE

Source: National Energy Board, Cushman & Wakefield Research

CANADIAN EMPLOYMENT - OIL, GAS, &

PIPELINE SECTORS

Source: Statistics Canada, Cushman & Wakefield Research

OIL PRICE VS. CANADIAN RENT CORRELATION

Source: EIA, Cushman & Wakefield Research

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

Q2 13 Q4 13 Q2 14 Q4 14 Q2 15 Q4 15 Q2 16

$ CDN per liter

0

50

100

150

200

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Thousand people

$14

$15

$16

$17

$18

$19

$20

$0

$20

$40

$60

$80

$100

$120

$140

2007

2008

2009

2010

2011

2012

2013

2014

2015

Q2-2016

sq ft per yr

$ per barrel (Brent)

Oil Price

Overall Office Rent

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2000

2002

2004

2006

2008

2010

2012

2014

May-16

Millions of bpd