25 / 36

25 / 36

Cushman & Wakefield

/

25

The oil industry

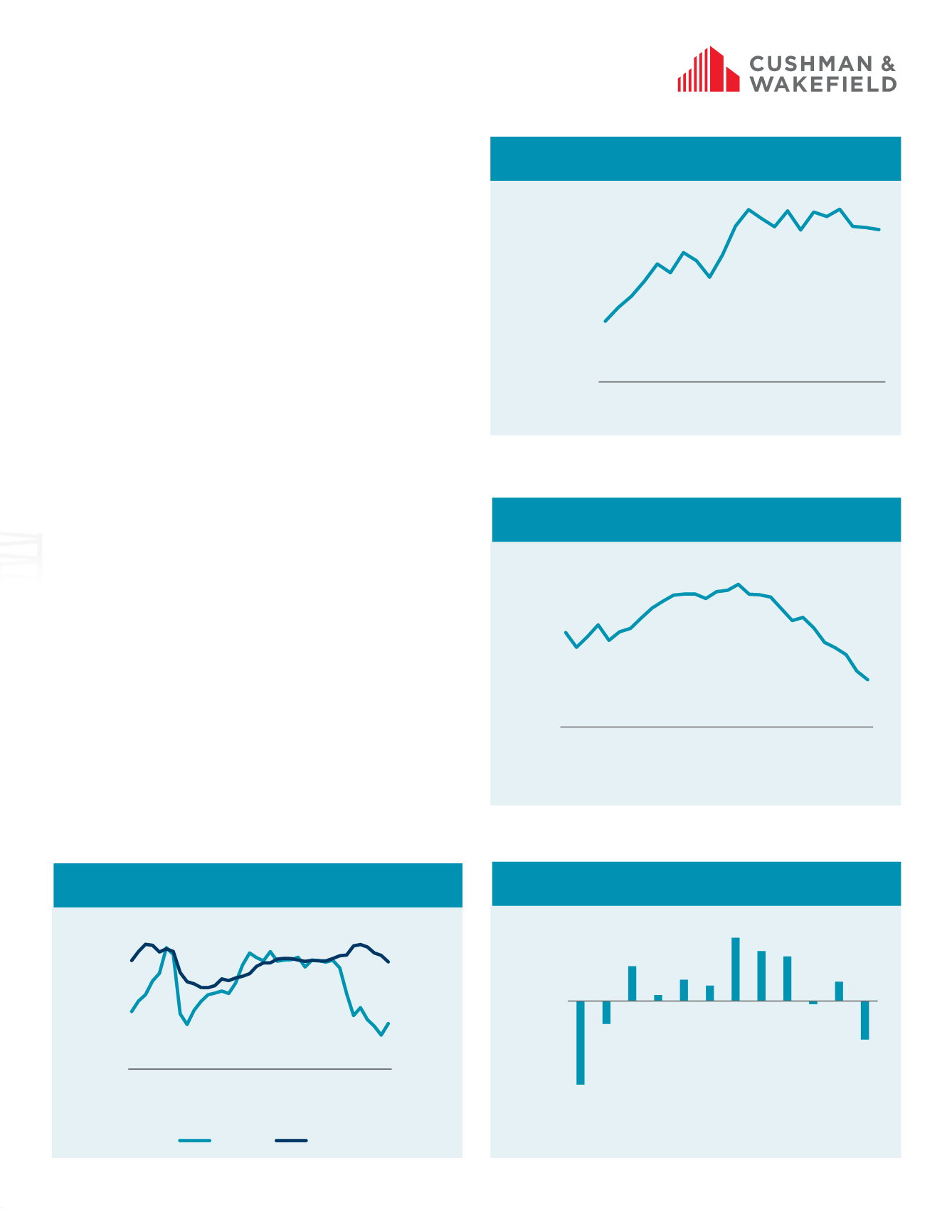

Oil production in EMEA reached 485 million bpd in 2014, 20% higher

than 20 years ago. However, there are some disparities at a regional

level. While Europe has seen a decrease in oil production of more

than 40% since the oil price bust, the Middle East and Africa have

seen increases of 38% and 19%, respectively. The Middle East is by

far the largest oil producer in the EMEA region, accounting for over

two-thirds of the supply in 2014. But Europe is the biggest source of

demand, consuming almost as much in petroleum and other liquids

as Russia, the Middle East, and Africa combined.

Energy employment

Energy employment has fallen across many EMEA cities — a trend

likely to continue. Moscow and Abu Dhabi employ the largest

number of energy workers at 90,000 and 60,000, respectively.

Energy-centric cities like Aberdeen, Stavanger, and Norway

employ less energy workers overall, but are still dependent on the

energy industry. Aberdeen employs 38,000 energy workers and

is eight times more dependent on the sector than the Scottish

national average, while Stavanger employs 10,000 energy workers

and is five times more dependent on the energy sector than

Norway as a whole. This leaves both cities vulnerable to oil price

fluctuations and associated pressure surrounding energy sector

employment. Cities with broader business sector employment,

including London, Oslo, and Rotterdam, are less dependent on the

performance of the energy market. In fact, these cities are likely

to benefit from lower oil prices as other industries are buoyed by

lower costs of production.

Office market outlook

Oil companies are weathering the fall in crude prices and its effect

on the economy, becoming increasingly conscious of both real

estate and staff costs. Energy sector demand for office space

across EMEA is likely to fall as a result, but the impact of this

will diverge at the city level. The Moscow office market has seen

rents fall by almost a third year-over-year due to the weakness

of the Russian economy brought about by lower oil prices, trade

sanctions, and increases in new supply. A continuation of these

factors means office take-up and rental growth will be below trend

next year. The high number of energy employees in Abu Dhabi and

the high proportion of energy employees in Aberdeen leave both

cities exposed to the risk of increased vacancy and flat-to-negative

rental growth. But the impact will be felt differently in less energy-

centric cities, including London. Such cities will begin to see oil

and associated companies attempt to reduce real estate costs,

though their diverse occupier base means the effect on the office

market will be limited.

EMEA OIL PRODUCTION

Source: EIA, Macrobond, Cushman & Wakefield Research

EMEA GAS PRICE

Source: Oxford Economics, World Bank, Haver Analytics, Cushman & Wakefield

EUROPE ENERGY SECTOR EMPLOYMENT,

ANNUAL GROWTH

Source: Oxford Economics, Cushman & Wakefield

OIL PRICE VS. EMEA RENT CORRELATION

Note: Rental is average rent for the seven tracked markets in EMEA

Source: EIA, Cushman & Wakefield Research

-80

-60

-40

-20

0

20

40

60

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Thousand people

0

100

200

300

400

500

600

700

$0

$20

$40

$60

$80

$100

$120

$140

2007

2008

2009

2010

2011

2012

2013

2014

2015

Q2-2016

GBP per sq m per year

$ per barrel (Brent)

Oil Price

Office Rent

$0

$2

$4

$6

$8

$10

$12

$14

2009 Q2

2010 Q2

2011 Q2

2012 Q2

2013 Q2

2014 Q2

2015 Q2

2016 Q2

$ per mil. BTUs

350,000

370,000

390,000

410,000

430,000

450,000

470,000

490,000

510,000

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Thousands of bpd

2015