33 / 36

33 / 36

Cushman & Wakefield

/

33

Energy producing provinces feel the bite

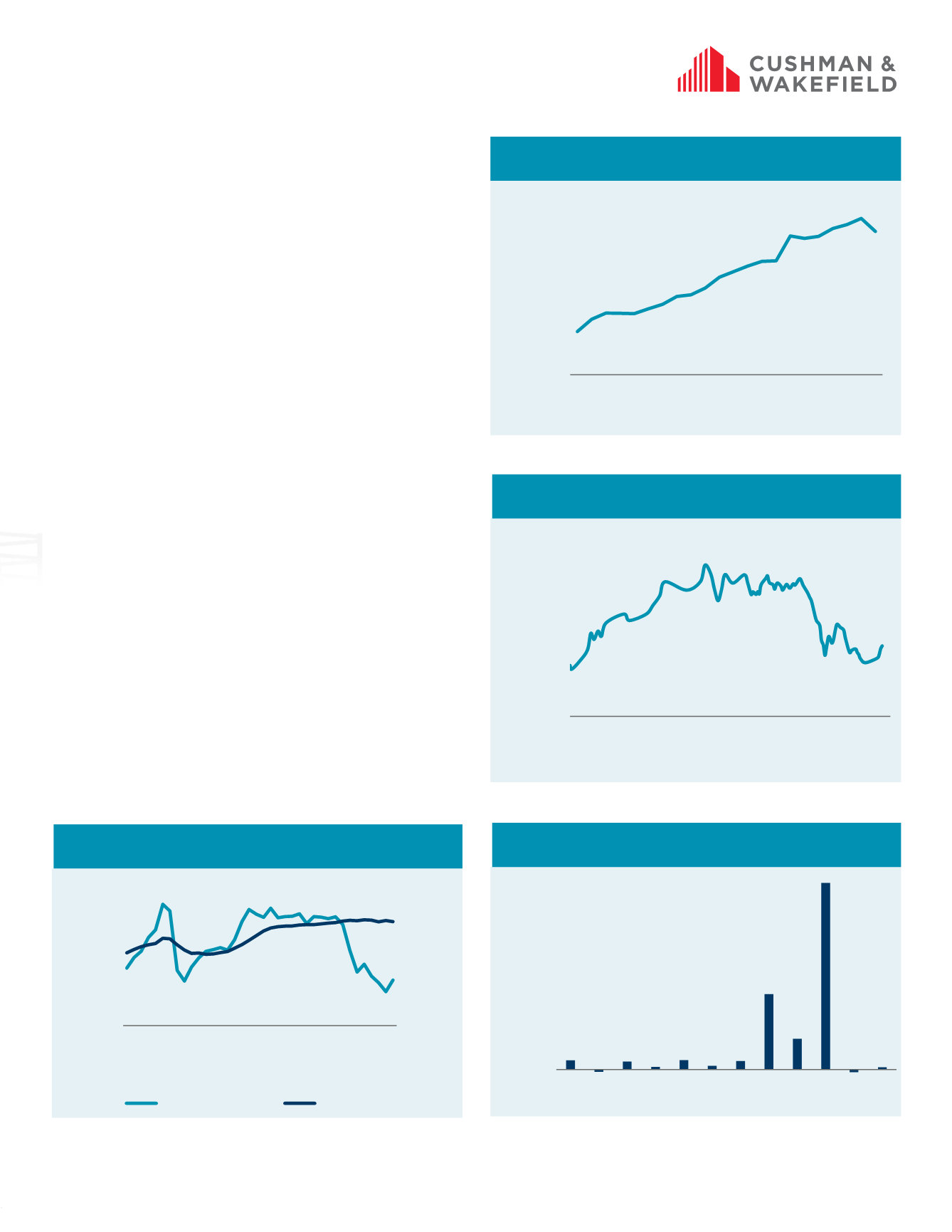

China is the world’s largest net oil importer and the second largest

oil consumer. Petroleum and total liquids production in China in

2014 was nearly 4.6 million bpd, a 50% increase from 20 years ago.

Recently, energy and production activity has been concentrated

in the offshore regions of the South China Sea and Bohai Bay, as

well as onshore regions in central and western provinces such

as Sichuan, Inner Mongolia, Gansu, and Xinjiang. China’s national

oil companies dominate the oil and natural gas upstream and

downstream market in the country. International oil companies,

however, do have access to the more technically challenging

onshore and offshore fields.

National and international HQs favor Beijing

Beijing is home to both the headquarters of China’s large national

oil companies and the China headquarters of international

oil companies doing business in the country. Other energy-

centric markets in the region are the preferred locations for

the divisional and sub-regional offices of both national and

international oil companies. But there are city-level specific

energy-centric markets. In Xinjiang, Karamay’s energy sector

accounts for a substantial 77% of overall city GDP. However, office

users in markets like Karamay tend to own rather than lease.

Other markets, specifically Dalian and Tianjin, not only boast a

significant energy component in their local economies, but they

also have established office leasing markets.

High prices – Dalian job growth; Low prices – Shanghai job growth

As oil prices rose prior to the end of 2014, energy sector-

dominated markets such as Dalian and Tianjin experienced the

largest job growth in percentage terms. When oil prices declined

in late 2014, job growth in both of these areas slowed sharply,

but remained positive. Conversely, non-energy centric cities such

as Shanghai saw significant job growth over that same period.

Benefiting from the net positive economic effects of cheaper oil,

companies in the non-energy centric markets consequently used

their profitability to raise headcounts in an attempt to gain greater

market traction.

Substantial office supply expected in coming years

In the next two and a half years, office supply is expected to

increase across a number of oil-centric markets in China, leading to

an increase in space availability.

CHINA OIL PRODUCTION

Source: EIA, Cushman & Wakefield Research

CHINA GAS PRICE

Source: National Development & Reform Commission, Cushman & Wakefield Research

CHINA ENERGY SECTOR EMPLOYMENT,

ANNUAL GROWTH

Note: 2015 figure is estimated

Source: National Statistics Bureau, Cushman & Wakefield Research

OIL PRICE VS. CHINA RENT CORRELATION

Note: Rental is average rent for the eight tracked oil markets in China

Source: EIA, Cushman & Wakefield Research

2,500

3,000

3,500

4,000

4,500

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Thousands of bpd

5,000

6,000

7,000

8,000

9,000

10,000

11,000

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

RMB per ton

0

50

100

150

200

250

$0

$20

$40

$60

$80

$100

$120

$140

2007

2008

2009

2010

2011

2012

2013

2014

2015

Q2-2016

RM per sq m per month

$ per barrel (Brent)

Oil Price

Office Rent

-100

0

100

200

300

400

500

600

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Thousand people